Electric vehicle batteries – controversies and solutions

By Jermaine Mensah, M&G Investments, as part of Tenet Compliance Services Adviser Development Programme

With road transport producing 16% of global emissions according to the IEA, the widespread adoption of electric vehicles (EVs) will be essential in global efforts to reach net zero. And yet, despite the sustainable credentials of EVs, there remain several environmental and social controversies around their production. Here, we review the main controversies in the EV battery value chain and the potential solutions.

The anatomy of an EV battery

Most EVs run on Lithium-ion (Li-ion) batteries – the same type of battery used in laptops and smartphones. The performance of batteries, including energy density (vehicle range) and the safety (flammability), is determined by the chemistry, with all chemistry mixes exhibiting different performance characteristics. For instance, Lithium Nickel Manganese Cobalt Oxide (NMC) batteries have high energy density due to the cobalt content of the cathode, which supports better driving distance range.

EV batteries work by circulating electrons, creating a difference in potential between two electrodes – one negative (the ‘anode’) and one positive (the ‘cathode’). These are immersed in a conductive liquid called the electrolyte. When the battery is powering the vehicle, electrons travel from the anode to the cathode, and vice versa when the battery is charging.

Anodes are usually made from graphite, whereas the electrolyte is a lithium salt in the form of a liquid or gel. The cathode is made from lithium metal oxide combinations of cobalt, nickel, manganese, iron and aluminium, and its composition largely determines battery performance.

Ethical problems in the supply chain

Cobalt gives vehicles the range and durability needed by consumers. EV batteries are the highest drivers of cobalt demand, consuming 34% of global capacity in 2021 (according to The Cobalt Institute). As EVs become more common, the European Commission and the Global Battery Alliance forecast a fourfold increase in cobalt demand by 2030.

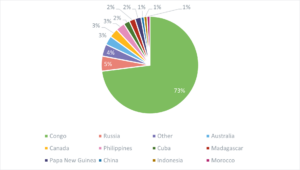

The sourcing of cobalt is closely tied to ethical controversies linked to child labour and slavery, which is arguably the most prominent issue when it comes to the EV battery landscape. The Democratic Republic of Congo produces more than 70% of cobalt globally, with 15-30% of mining production capacity attributable to artisanal and small-scale mining (ASM). This makes cobalt production from ASM the second largest cobalt-mining sector in the world after LSM (large-scale industrial mining) production in the DRC. ASM has been linked to child and slave labour, and UNICEF estimates that more than 40,000 children currently work in the artisanal and small-scale mines.

As widespread adoption of EVs continues, cobalt mined from artisanal miners is mixed into the EV production value chain. It is impossible to determine how much of the EV battery production pumped out today is linked to artisanal miners, but it is safe to say this is a major ethical controversy that persists.

Where does cobalt come from?

Source: United States Geological Survey and Bernstein analysis, 2022.

Environmental damage from mining

Alongside the social controversies, there are also environmental issues from the extraction of key minerals such as lithium and nickel. According to McKinsey & Co, growing electric vehicle use is expected to increase lithium production by approximately 20% a year this decade, and by 2030, EVs will account for 95% of lithium demand.

Lithium is extracted from either hard rock or underground brine reservoirs. Hard rock extraction produces 15 tonnes of CO2 emissions per tonne of lithium, and leaves scars on the landscape. It has also been linked to water contamination in Tasmania, an Australian mining hub.

Brine extraction creates 5 tonnes of CO2 emissions per tonne of lithium. It is a water-intensive process – seawater and other surface water are mixed with freshwater and left to sit in ponds for up to 18 months, leaving behind minerals as the water evaporates. The practice has been linked to water shortages in Chile, where water availability has dropped to 10-37% over the past 30 years, and is forecast to get worse.

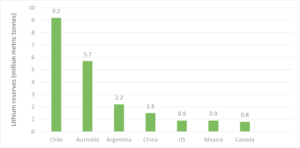

Lithium reserves are concentrated in Latin America and Australia

Source: United States Geological Survey, MineSpans, 2022.

Nickel is a key element used in the chemistry mix for Nickel Manganese Cobalt (NMC) and Nickel Cobalt Aluminium (NCA) Li-ion batteries, which contain 33% and 80% nickel respectively. Nickel mining has the highest emissions intensity of all metals, producing an average of 10 tonnes of CO2 per tonne of metal. The practice has also been linked to increased deforestation and the contamination of local rivers and lakes in Indonesia, which has the world’s largest nickel reserves.

Safety concerns

In the same way that smartphone batteries can get hot when charging, EV batteries are naturally prone to overheating. Of course, this poses serious health hazards or potentially life-threatening risks to the end user if the batteries catch fire.

This has led to a number of high-profile product recalls. For example, General Motors recalled 73,000 Chevrolet Bolt cars after at least 13 vehicles caught fire due to ‘rare manufacturing defects’. Hyundai also recalled 74,000 of its Kona EVs after 16 of them caught fire. In both cases, the batteries were produced by LG Energy Solutions (LGES).

However, it is important to bear in mind that the recalls are immaterial in comparison with the millions of units sold by LGES each year. Furthermore, recalls for safety reasons are not so uncommon, and were occurring for internal combustion engine vehicles before EVs. As an example, in 2022, Volkswagen and Audi recalled more than 225,000 vehicles due to safety concerns over faulty tire pressure monitoring systems.

What are the potential solutions?

The EV battery production industry is in its early days, and is constantly evolving. While there is no one-size-fits-all option, there are various potential solutions to each of these controversies. Here, we explore some of them in more detail.

Recycling

Battery recycling will play a key role in improving the ethical and environmental impacts of the EV battery supply chain. 2030 is anticipated to be the year that we see an influx of recycled batteries pumped back into the supply chain, as batteries manufactured between 2017-22 finish their 10-year life cycle.

It’s difficult to put a number on expected recycled percentages, as regions have different targets and regulations. Currently, within the EU, the recycled content of batteries is only 12 % for aluminium, 22% for cobalt, 8 % for manganese, and 16% for nickel. However, with new EU regulations these numbers are set to increase (see below for more information). Research from Goldman Sachs estimates that more than 50% of lithium and nickel in the European EV market will come from recycled batteries by 2040.

It is worth noting that recycling rates will also depend on battery chemistry, with some easier to recycle than others. Furthermore, many batteries have been designed without consideration for recycling, and it can be difficult to extract the raw materials. A lack of recycling regulations prior to 2020 meant that manufacturers had no incentive to make their batteries easily recyclable.

The evolving regulatory landscape

Evolving regulations will be essential to overcoming the social and environmental problems. The EU has proposed a set of regulations to encourage greater recycling and environmental transparency. It includes quotas for minimum recycled content of new batteries – at least 12% of cobalt, 85% of lead, 4% of lithium, and 4% of nickel must come from recycled sources.

The regulation also includes new targets for recovering used batteries. For waste portable batteries, this is 45% by 2023, 63% by 2027 and 73% by 2030, and for ‘light means of transport’ batteries, this is 51% by 2028 and 61% by 2031. Furthermore, EV manufacturers must declare carbon footprints and comply with maximum lifecycle carbon footprint thresholds.

In the US, the almost-$400 billion Inflation Reduction Act legislation offers EV manufacturers tax credits if at least 50% of components are manufactured or assembled on US soil, or if at least 40% of the battery mineral contents are extracted, processed or recycled in the US or countries which have a free trade agreement with the US. This is expected to promote a better domestic supply chain for EV batteries, with a greater ability to understand and track the source of raw materials, and reduce reliance on countries with human rights issues.

Other battery technologies

There are alternative battery chemistries emerging, which negate the above problems to varying extents. It’s important to note that there is not yet an alternative to Li-ion batteries with equal energy density, which can be rolled out commercially at scale. Energy density determines the EV’s range – so this will be a crucial challenge to overcome if we are to see alternative batteries take dominant positions in the global market. However, some of the most promising contenders are:

Lithium-iron-phosphate (LFP)

LFP batteries are becoming popular in EVs from European manufacturers. They contain no cobalt, instead using iron and phosphate, which are cheaper, more abundant materials. The batteries have less energy density, but better thermal safety than Li-ion batteries. Tesla now uses LFP batteries in its standard Model 3 and Model Y cars, which have lower range requirements.

Sodium-ion (SIB)

This early-stage technology is not yet commercialised. It uses aluminium, and sodium, which is more than 1,000 times as abundant as lithium. However, SIB batteries have less energy density/vehicle range than Li-ion batteries, and are heavier, making them less suitable due to their considerable size.

Solid-State

At a very high level, solid-state batteries use a solid electrolyte as opposed to the liquid or polymer gel found in current Li-ion batteries. This can take the form of ceramics, glass, sulphites or solid polymers. These batteries do contain cobalt, but much lower amounts than Li-ion batteries, and offer advantages for power density and lower risk of fire. Many manufacturers, including Toyota, Samsung and LGES, are aiming to reach commercialisation for solid-state batteries over the next few years.

In conclusion

EVs will undoubtedly help to decarbonise the global economy, and their widespread adoption will play an integral role in efforts to reach net zero emissions. However, while the industry is continually evolving, there remain fundamental social and environmental issues which must be tackled.

The value of investments will fluctuate, which will cause fund prices to fall as well as rise and investors may not get back the original amount invested.

For financial advisers only. Not for onward distribution. No other persons should rely on any information contained within. This financial promotion is issued by M&G Securities Limited which is authorised and regulated by the Financial Conduct Authority in the UK and provides ISAs and other investment products. The company’s registered office is 10 Fenchurch Avenue, London EC3M 5AG. Registered in England and Wales. Registered Number 90776.